Sales Revenue Journal Entry Bookkeeping Example Explained

The original sales journal entry is the same as the periodic inventory system. So you give them a discount of 20% to make up for the inconvenience, making the final sale price $40. This can be a bit confusing if you’re not an accountant, but you can use this handy cheat sheet to easily remember how the sale journal entry accounts are affected.

Do you already work with a financial advisor?

Both sales returns and allowances represent a reduction in a company’s revenues after it makes sales. The accruals concept requires companies to account for revenues when they occur. Therefore, companies must not treat these transactions on cash settlement. Usually, companies record sales in the books when they deliver goods to customers.

How to Record a Sales Revenue Journal Entry

In this entry, the sales returns and allowances account is debited and the accounts receivable account is credited. When customers return merchandise sold for cash, the sales returns and allowances account is debited and the accounts payable account is credited. Sales returns are goods that customers return to a company due to various reasons. Sales allowances are discounts offered to customers after a company makes sales.

Cash Sales Journal Entry

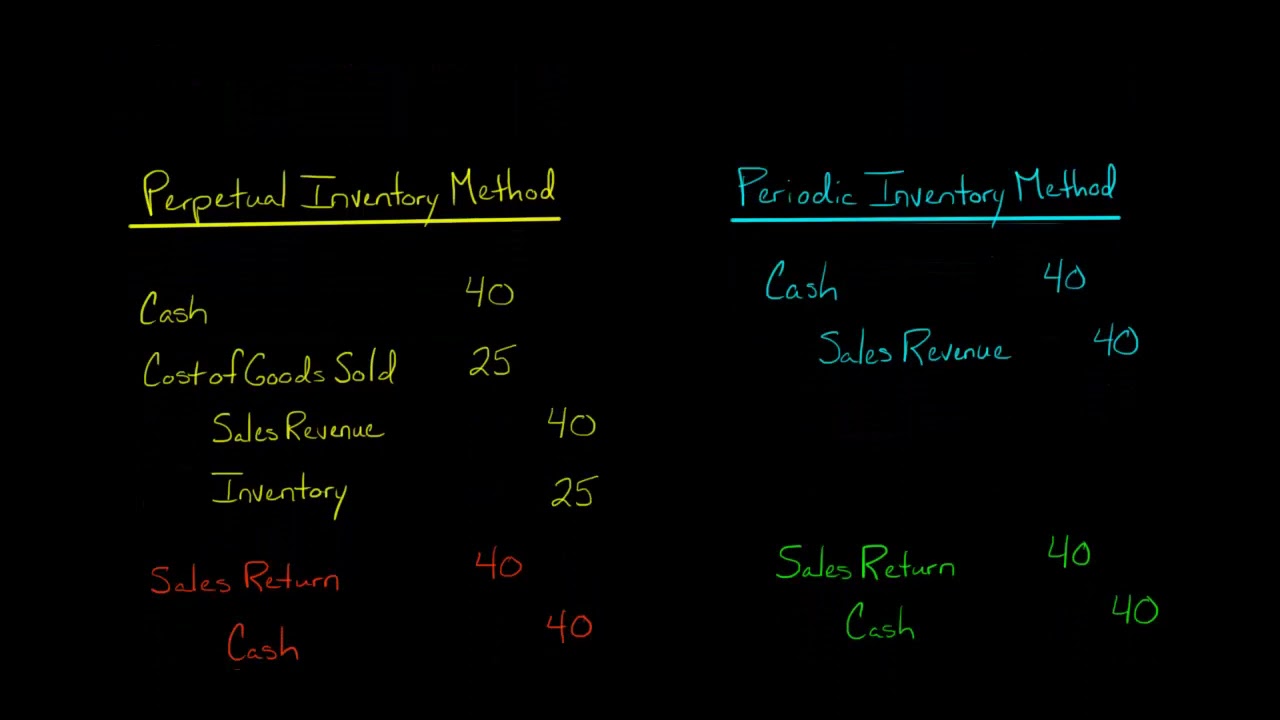

Here are a few different types of journal entries you may make for a sale or a return depending on how your customer paid. If your customer purchased using a credit card, then you use accounts receivable instead of cash. That’s because the customer pays you the sales tax, but you don’t keep that amount. Instead, you collect sales tax at the time of purchase, and you make payments to the government quarterly or monthly, depending on your state and local rules. If the customer’s original purchase was made using credit, you recorded the original sale by increasing your Accounts Receivable account through a debit. Since the ledger accounts are closed to the General Ledger, this account balance indicates that there are no more invoices in which credits have not been posted.

- Now, Jenny must record this amount to ensure her financial statements reflect the true picture of her business.

- On 1 July 2014, it sold 500 footballs each to Club A and Club B at a price of $20 per football.

- However, some customers found problems with their lamps and returned them.

- This account has a negative or debit balance, so it is also called a contra-revenue account.

Journal Entry for Credit Sale:

Similarly, a sales allowance does not entail a discount for an early payment, which is what cash discounts are. Purchase returns are items that are returned by the customer after purchasing, while sales returns are items sent from a wholesaler back to their supplier. By understanding these journal entries and taking proper steps when issuing refunds/credits, businesses can ensure that their accounting records remain accurate and up-to-date. It is very important for the management to review the information regarding the sales return. This is due to a big volume or amount of sales return transactions can suggest various problems that may prevent the company from achieving its goal.

They are used to record product returns and allowances issued to customers. For this, businesses deduct the amount identified under the returns and allowances head from the gross sales figure, and the net sales figure is derived from this calculation. There are two approaches for making journal entries of transactions related to sales returns and allowances. A company may choose any approach depending on its volume of returns and allowances transactions during the year. The first approach is to record returns and allowances in the general journal, which is appropriate for companies with only a few returns and allowances during the year. The second one is to record these transactions in a special journal known as the sales returns and allowances journal.

Debits and credits are equal and opposite, so when you increase an account using a debit, you must decrease another with a credit. One of the most common reasons for product returns is when customers find that the item they are receiving does not match the product description. A company, ABC Co., sold goods worth $100,000 to another company, XYZ Co. Companies may offer sales allowances for various reasons, which include the following.

We will need to keep the returned goods in the company’s warehouse and reflect this transaction correctly in the accounting records. In instances where goods are returned or allowances are made, the Sales Returns and Allowances account, a contra-revenue account, is used to adjust the sales revenue. In the section below, section 1256 contracts we illustrate how the sales return and allowances are recorded in both perpetual and periodic inventory systems. When merchandise is returned, customers usually ask for a cash refund. However, a customer may find that low-quality (or slightly damaged) goods can be resold at a lower price or they can be used elsewhere.

During this process, the goods may go under physical changes or deformities. Once customers receive the products, they may not work as intended or suffered damages. In exchange, the company will compensate the customers by repaying them or selling them other products.

11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. When posting to the accounts receivable controlling account, the account number of accounts receivable (112) was written to the left of the diagonal line. Return of merchandise sold for cash is entered in the cash payments journal or cash book.